Financial Analyst

Tosee Modiriat Rahbordi Amin (Amin Strategic Management Development) TehranPosted 4 years ago

Job

Company

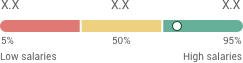

Salary

Applicant Insights

Employment type

- Full Time

Educations

Seniority

Similar Jobs

To see more jobs that fit your career

Jobs and employment for Iranian

professionals.